Real Estate Investing and Your Personal Financial Planning

Real Estate Investing And Your Personal Financial Planning

Often we see polarization among the investing public between those that invest and focus their financial planning primarily in the liquid securities markets and those that invest primarily in real estate. Our view is that under certain circumstances, liquid securities investing and illiquid real estate investing can be complementary. However, the key to navigating between these areas is having an appropriate framework for how to think about investing in real estate in the context of personal planning goals, risk management, liquid investing, tax planning, and estate planning. Admittedly, we are not day to day real estate investing experts, but here are some considerations when it comes to real estate investing in the context of your personal financial planning.

Evaluate Your Overall Balance Sheet As You Consider Real Estate

Before moving forward with allocating a large portion of one’s net worth into real estate, we recommend having a financial plan around the optimal mix of assets on your balance sheet. Assets on one’s personal balance sheet can generally be divided into three categories and each of these categories can enable the achievement of particular goals: 1) safety assets like cash in checking accounts and your personal residence are meant for essential goals like living expenses and shelter; 2) market assets like stocks and bonds are earmarked to achieve must-have goals like retirement and college education funding; and 3) moonshot assets like private equity, cryptocurrencies, equity compensation stock options, and investment real estate are meant to fund aspirational goals like funding early financial independence or buying a second home.

It's important to remember that when one moves from assets predominantly held in the safety and market buckets to the moonshot bucket, one is taking on more risk with diminished diversification and illiquidity. The optimal balance between these three buckets is highly dependent on your personal circumstances, but a prudent mix in your 50’s could be one-third in each bucket.

As you allocate between the three asset buckets, your moonshot bucket and market bucket assets shouldn’t be framed as zero-sum trade-offs between each other, they actually complement each other. The stock assets in your liquid bucket could be a source of capital or collateral in case of an unforeseen capital improvement outlay needed in your real estate portfolio. On the other hand, your real estate portfolio can serve as a hedge by having accelerating rental income (I’m looking at you, New York City rental real estate in 2023) to offset inflationary pressure and increased volatility on your stock portfolio.

Pin Down Your Real Estate Goals, Investment Thesis, And Comparative Advantage

Once you’ve decided the optimal amount of real estate on your balance sheet, having clear real estate goals, a solid investment thesis for each potential investment property, and developing the specific comparative advantages needed to execute can help maximize returns over the long-term. Are you looking for long-term price appreciation to combat inflation by buying undervalued single-family residential properties in communities with surging favorable long-term demographics by raising capital through family and friends? Or perhaps you’re looking to collect income in retirement by buying a portfolio of modestly priced multi-family units which you can manage at low cost relative to other investors with a network of real estate support professionals and low cost financing? Each of these strategies requires disparate skills and focus to evaluate investments, decide which properties you deploy capital in, execute ongoing management, and one day profitably exit. Being clear on what your specific strategy is and how you execute on that strategy is key to financial planning success.

While diversification is a key tenet of successful investing, dabbling between various types of real estate investments can lower your chance of success. Rather than shifting the strategic focus between many different property types with the aim of diversification, we suggest garnering portfolio diversification by complementing a focused real estate strategy with a diversified portfolio of liquid stocks and bonds.

Gauge Your Personal Suitability For Real Estate Investing

Many people are drawn to real estate investing with the goal of “passive income”, but the reality is that successful real estate investing usually takes a significant amount of time and knowledge to implement consistently. We’ve seen clients spend years building up a profitable portfolio of investment properties with the aim to fund a comfortable retirement of passive income, only to switch gears and hastily monetize the portfolio after growing tired of managing repairs and collecting checks. Personal preferences and taste can derail a perfectly conceived and executed financial plan.

While real estate is “passive income” from an IRS perspective, real estate investment and management for many is anything but a passive experience. Since it’s costly to switch on and off a long-term real estate investment strategy due to transaction costs, we recommend starting small and building over time to gauge your personal tolerance and aptitude for investing the appropriate amount of time and effort necessary to complement your overall wealth management strategy with real estate. Obviously, there are management companies that you can engage to take some of the administrative burden of real estate investing. The quality and cost of these services can vary widely, so it’s important to tread carefully.

In addition to understanding your personal suitability for real estate, we recommend that investors understand their personal “why”, so that their investments can dovetail with their values and goals. It might make sense to do a value exercise with clients where you write down a broad array of values (family, impact, freedom, etc.), and then narrow down the most important values down to 10 and then to 5. Consequently, once values are defined, investors can more easily set financial goals and allocate capital among investments that align with their values. For example, if you have a goal of living overseas in retirement, you might want to think twice before building a large rental real estate portfolio domestically given the complexities of managing that portfolio out of the country. Moreover, in that situation you’d have a currency mismatch risk as you earn dollars from real estate and pay for expenses in a foreign currency.

Understand the Trade-offs between Real Estate and Liquid Investments

Oftentimes we see investors evaluate the merits of potential investment real estate opportunities purely against the relative return they’ll receive from liquid investments. This approach can be dangerous given the differences between liquid and illiquid investments. One might estimate that a real estate property will have an estimated internal rate of return (IRR) of 12%, so they might move forward with the investment since that exceeds their expected stock market return hurdle of perhaps 8% or an expected diversified portfolio hurdle rate of stocks and bonds of 6%. We would argue that investors should consider several adjustments when evaluating real estate investments relative to liquid investments. For example, you might add 4% to your hurdle rate as an “illiquidity premium”, add 3% to your hurdle rate since real estate investments have a diminished ability to easily diversify given the high required minimum sizes, and add another 2% to compensate you for your time and personal liability. In this example, as you model a potential real estate investment, you might require a minimum 17% internal rate of return (8% + 4% + 3% + 2%) to allocate capital away from liquid investments.

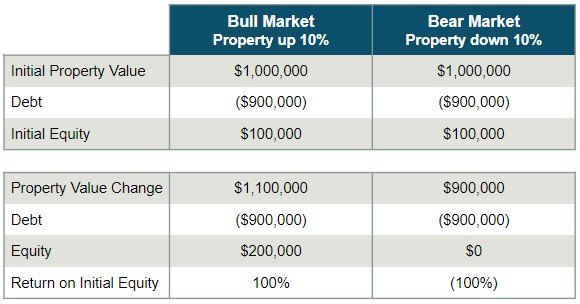

One of the unique features of real estate investing is the ability to leverage investments at a level much higher than liquid investments like traditional stocks or bonds. As a result, real estate offers investors the ability to enhance returns through leverage, but it also opens the door for potentially significantly more risk. For example, if you buy a property for $1,000,000 with only 10% down, your return on capital invested if the property goes up 10% and you sell and pay off the debt is 100%. On the flip side, you lose 100% if the property goes down 10% in this scenario. With this in mind, it’s important to evaluate real estate projects on their merit on a leverage adjusted basis. A 10% IRR project with no leverage could be a better debt-adjusted project than a 15% IRR project with leverage.

A Long-Term Time Horizon Can Mitigate Real Estate Risk

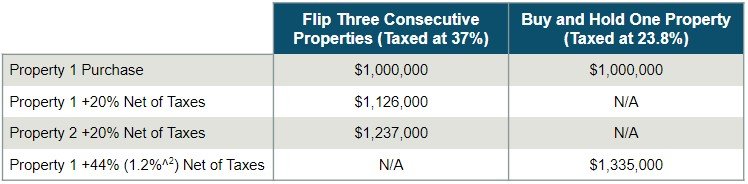

Just like in the stock market, a long-term time horizon can mitigate some of the risks in real estate, particularly with leverage. The many months from the time one decides to sell a property to actually having the cash on hand, can help avoid emotional selling that we often see with many stock investors. Forced selling with high leverage is a recipe for disaster, so having a long-term time horizon to avoid selling during real estate market pullbacks can help mitigate risk and facilitate effective wealth management. Moreover, given the high transaction costs of purchasing and selling real estate, amortizing these expenses over many years can increase your chances of a higher return. Many of the favorable tax benefits investors are enabled by a longer term time horizon. For example, long-term capital gains rates between 0% and 23.8% await real estate investors when they sell properties held for longer than one year, while short-term real estate flippers could face Federal tax rates up to 37% or even higher if the laws aren’t changed before 2026.

A real estate investment flipper that invests $1,000,000, earns a 20% return, then reinvests the after tax proceeds earning another 20% return in a second property would have $1,237,000 after taxes if taxed at short-term capital gain rates. A buy and hold strategy that has the same gross returns but is taxed at long-term capital capital gains rates would have $1,335,000 after taxes. A buy and hold strategy vis-a-vis a real estate flipper strategy is even more attractive taking into account buy and sell transaction costs, particularly in areas like New York City that have higher than typical real estate transaction costs.

Be Disciplined about Modeling Future Real Estate Returns

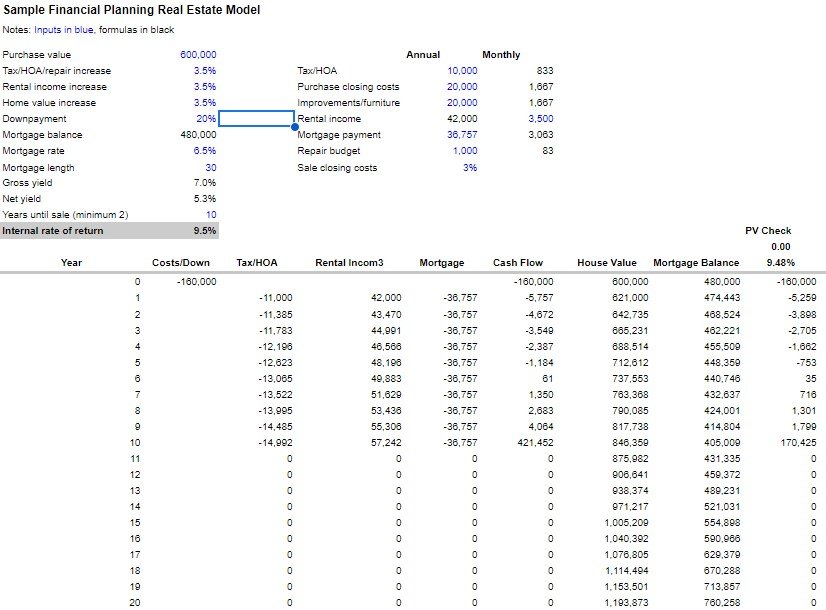

Too often we see investors identify a property they like, estimate how much they can rent it out for, obtain a mortgage quote and then move forward because it’s “cash flow positive” without rigorous forecasting about what their expected return will be. Alternatively, we highly recommend investors develop a robust financial model calculating IRR based on rigorous research on the project’s assumption. The model should have estimates for rental increases, vacancy, repairs, capital projects, and other key inputs. Each one of these assumptions should be adjusted up and down to see how impactful it is on the IRR. What if the financing rate goes up 2%. What if there’s a big renovation needed in year five? Your model should be able to answer these and other questions to determine the attractiveness of the investment. For example, we’ve found that the ability to push through annual rental increases, even modest increases, can have a profound impact on your IRR. For example, increasing monthly rent of $5,000 will be $7,241 after 15 years of annual 2.5% increases, while increasing the same $5000 rent by 10% every five years results in a monthly rent of $6,655 after 15 years.

Understanding Real Estate Financing Types and Their Implications

Optimal financing is a huge determinant of real estate investing success, so understanding the trade-offs and implications of different financing structures and types should be a key component of any real estate financial plan. For example, shorter amortizations can lower the overall interest rate costs of a property assuming an upward sloping yield curve, but could put pressure on cash flow as greater amounts of principal are due sooner. In general, we’re a fan of longer term amortizations that give budget relief, but also give the flexibility to prepay amortization and essentially reduce the amortization term at the investor’s discretion. The initial amount down on a property also can impact the overall success of a real estate investment. Our general preference is to put more down in higher interest rate environments and minimize the amount down in low interest rate environments. In low interest rate environments, the spread between the interest cost and the opportunity cost is wider. Consequently, if would-be higher down payment amounts can be invested at rates of returns higher than the interest costs, the balance sheet will be positively affected over the long-term. That being said, if lower down payment amounts are sought primarily because a property is out of reach financially, the risk to one’s overall personal financial planning may necessitate avoiding the investment altogether.

Real estate investors should be keenly aware of the implications of debt not just in their real estate portfolio, but throughout their personal balance sheet. If you’re putting less money down on your investment properties, it likely doesn’t make sense from a risk management perspective to run a meaningful margin balance in your brokerage portfolio or borrow from your 401(k).

Take Advantage of Tax Savings When Buying Real Estate

The tax code provides a spectrum of tax opportunities throughout the lifecycle of an investment in real estate. A solid team advising you can help reduce your tax liability potentially even during the initial real estate purchase. For example, it’s often advisable for investors to do property renovations after the property has been put into service as a rental. As such, expenses incurred during the renovation could be expensed to lower your taxes in the year of purchase instead of being added to the property’s cost basis. The time value benefit between lowering your taxes through expensing renovations right away versus having a higher basis and consequently a lower capital gain when you sell the property down the line can be significant. As well, investors should investigate the evolving property specific tax benefits available, like energy credits.

Have a Plan to Garner Tax Savings While Managing Your Real Estate

As an investor manages their property, it’s imperative that they work with their team to evaluate the various tax opportunities available. As homeowners transition into investment real estate, the menu of tax deductible expenses expands with insurance, homeowner association fees, repairs, and other expenses. Real estate for some becomes a way to circuitously remove the $10,000 TCJA SALT limitation as investment real estate taxes become fully deductible.

Generally, real estate investment income is going to go on your Schedule E, which can be a huge plus since this income is not subject to FICA taxes. Solid recordkeeping can make your life easier, and it usually makes sense to get comfortable keeping records in the expense categories on Schedule E, and knowing which expenses can be expensed and which ones have to be added to your cost basis.

For some investors, real estate can be a way to shield non-real estate income. For example, rental real estate losses up to $25,000 can be applied to ordinary income up to income phase outs of $150,000 of adjusted gross income. Even if you are above that income threshold, real estate allows you to carry forward losses to other years and offset real estate income to lower your tax liability in future years. Another way to offset ordinary income, or income of your spouse, with real estate losses, is to qualify for real estate professional status. However, the qualifications are rather stringent as you would have to “materially participate” in real estate activities by spending at least 750 hours or more managing the real estate and have real estate management be your primary career. There are numerous potential landmines in effectively qualifying for this benefit, so work closely with your team of advisors if you are considering this.

In some areas, real estate owners can challenge their property tax assessment and reduce their tax bills. In New York, real estate owners, usually by working with an attorney can go through the “tax certiorari” process and challenge their tax assessment by arguing that the assessment is misclassified, unequal, or excessive.

Optimize Depreciation Strategies to Enhance Returns

Arguably the most profound tax benefit for real estate investors is depreciation, so it behooves investors to have at least a novice understanding in this area. Our tax code allows the theoretical “cost” of depreciation to be applied against actual real estate cash flow. In essence this allows for many properties with positive cash flow to show a loss for tax purposes, resulting in substantial tax savings. For example, a residential real estate rental property purchased for $1,000,000 earning $40,000 in cash flow per year could pay taxes on only less than $4,000 of income since a depreciation expense of ~$36,000 ($1,000,000 divided by the allowable useful life of 27.5 years).There isn’t a free lunch though, since the depreciation expense taken along the way is “recaptured” as a taxable expense when the property is sold. However, the time value of delaying that tax liability by many years can be positively impactful to the investment’s IRR. We would advise real estate investors to work closely with their CPA and financial planner to investigate the pros and cons of the full spectrum of depreciation opportunities, including bonus depreciation, cost segregation studies, and other options.

Understand Unique Tax Attributes of Short-Term Rentals

Usually, short-term rental income like Airbnb income is Schedule E income, which benefits from self-employment taxes not being levied against it. Some people may conversely prefer this income captured on their Schedule C since that would allow retirement plan contributions, losses to more easily offset other income, and more favorable status with lenders. However, Schedule C treatment on short-term rental income requires providing substantial services so it’s best to discuss any short-term real estate income with your tax adviser.

Tax Savings Selling Real Estate

There’s a continuum of tax saving options real estate investors have when selling their property. A Section 1031 exchange can allow investors to defer payment of capital gains on the sale of an investment property if another property is identified and purchased within specified guidelines, which can enhance your IRR. However, we’ve seen many investors overpay on the reinvestment property given the reinvestment time pressure, so it’s important to not let the aim of lower taxes facilitate a suboptimal investment. Another alternative is for investors to defer real estate capital gains until 2027 through reinvestment of capital gains into an opportunity zone fund. As an additional benefit, subsequent gains are free from taxation if you hold the investment for more than ten years. A more traditional strategy to lower tax liability when selling a property is to use the installment sale method, which recognizes the capital gain over many years. Spreading the gain over many years can lower the capital gains bracket you incur vis-à-vis paying the capital gain in the tax year of the initial sale, but an installment sale can also introduce credit risk as the seller initially essentially finances the buyer’s purchase over several years. Moreover, depreciation recapture is due in the year of the initial sale resulting in a possible large tax bill in the initial year of the installment sale.

Prioritize Risk Management with your Real Estate

It can’t be emphasized enough that an effective real estate investment strategy must be accompanied by a prudent risk management strategy for both the probable and long-tail risks unique to real estate. A sizable emergency fund, access to capital, and adequate property insurance are table stakes for an unforeseen risk like an urgent renovation on a property’s pipes due to a colder than expected winter. Natural disasters are increasingly frequent, so not only is adequate coverage an area to focus on, but real estate owners must have a plan around insurance carriers drastically increasing their premiums, dropping coverage on your property, or leaving your real estate market entirely.

In an increasingly litigious society, investors should also have a comprehensive multi-pronged legal protection strategy. Personal umbrella insurance covering your total net worth is a relatively low cost protection strategy for starters. As well, you could work with your attorney to set up an LLC for each property you own. If someone is injured on your property and sues you, it’s an arduous process for them to receive a charging order on your property and to get actual distributions from you under this and other structures. There’s a spectrum of asset protection including trust structures, equity stripping, and other strategies, so it’s best to get the various members of your team, including your CPA, insurance broker, financial planner, and attorney, engaging in strategic conversations to determine the optimal cost effective structure for your circumstances.

Consider the Local Risks

Real estate owners should also consider that some areas relative to others will have inherently more risk due to local laws and regulations. States like California and New York have favorable tenant laws at the expense of landlords. This can be problematic for a real estate investor when, for example, a tenant is not paying rent and you attempt to replace that tenant with a new one. Likewise, some areas have more favorable zoning laws. Understanding the local regulations and laws related to your investment property is key to mitigating risks.

Tread Carefully with Real Estate in an IRA

While some investors advocate for buying real estate in a self-directed IRA, this strategy can backfire. There are numerous limitations and various prohibited transactions when implementing this strategy, and the IRS could assess large tax penalties for violating them. Related party transactions, personal use of the property, and financing could all be problematic when buying real estate in your IRA. It could also be challenging to complete required minimum distributions (RMDs) with illiquid real estate in your IRA, especially since by the time an investor has critical mass to buy real estate in their IRA, they’re probably on the older side. Also, many of the fundamental tax benefits of real estate like depreciation and emphasizing long-term capital gains over ordinary income are rendered useless in an IRA structure, so you might want to consider other high growth assets for your IRA.

Reassess Your Estate Planning When Investing in Real Estate

There are a myriad of considerations and strategies that could impact your estate planning when you own real estate, so it’s important to get your estate planning attorney talking to your CPA and financial advisor to think through the issues. Effective transfer of your wealth at your passing, minimizing taxes, avoiding probate, implementing asset protection, and maximizing charitable intent could all be affected by your real estate strategy. One frequently used strategy involves transferring highly depreciated (low cost basis relative to market value) real estate assets from one generation to the next at the passing of the first generation rather than being gifted during their lifetime. This allows for a step-up in basis to market values at death and diminishes capital gains for the second generation. Another potential issue that could be averted with proper planning is that properties held in multiple states could necessitate your heirs initiating multiple state probate proceedings, which would cause additional administrative burdens precisely when the family is going through a difficult time.

David Flores Wilson and Dann Ryan are New York City-based CERTIFIED FINANCIAL PLANNER™ Practitioners & Managing Partners at Sincerus Advisory. Click here to schedule a time to speak with us.